Investing is fundamentally about managing the relationship between risk and return. In Pakistan, this balance is influenced by local economic conditions, inflation, interest rates, exchange rate fluctuations, and investor sentiment.

As of mid-2025, Pakistan’s economic environment has shifted significantly from the high-inflation, high-rate crisis of 2023, with inflation reaching as high as 28.3% in 2023, policy rates climbing above 22%, and a currency that has lost more than two-thirds of its value over the past decade. The country has experienced a sharp easing of monetary policy, a decline in inflation, and stabilization in the currency However, investors still face complex decisions about where to invest their money, and understanding real, current risk-adjusted returns is crucial.

In many developed economies, risk and return often seem predictable, but in Pakistan, they can shift rapidly with macroeconomic shocks. For investors here, understanding risk and return is more than theory—it’s survival.

The Macro Backdrop: 2023 Crisis to 2025 Stabilization

Pakistan experienced a severe inflationary and currency crisis in 2023; consumer price inflation averaged around 28.3% for the year, with a monthly peak of 38% in May (Pakistan Bureau of Statistics). The State Bank of Pakistan’s policy rate reached a record high of 22% in June 2023 (SBP). Meanwhile, the rupee depreciated sharply, crossing PKR 307 per USD in the interbank market in September 2023 (SBP exchange rate data).

Since then, a combination of IMF-backed stabilization policies, tight monetary conditions, and fiscal consolidation has cooled inflation and restored partial confidence in the rupee. As of June 2025:

SBP Policy Rate: 11.00%

CPI Inflation: 3.2% (June YoY)

USD/PKR Official Rate: 283.76

This represents a dramatic normalization from the crisis period. However, structural vulnerabilities remains, including external debt repayments, a thin forex reserve buffer, and political volatility. For investors, these factors shape both opportunities and risks.

Understanding Risk and Return

In basic terms, return is the gain from an investment, often expressed as a percentage. Risk is the uncertainty of that return—how likely it is that you will earn less than expected or even incur a loss.

In Pakistan, even traditionally safe options like government securities come with the risk of being eroded by inflation. While equities can offer high returns, they are equally prone to volatility. Currency depreciation poses yet another layer of risk that can silently reduce real returns, even when your investments are seemingly growing.

Understanding this risk-return balance is essential. When making investment decisions, you must think beyond nominal profit percentages and consider factors like inflation, interest rate shifts, currency trends, and political uncertainty. Your investment decisions must reflect both your goals and your ability to weather financial ups and downs.

Nominal vs. Real Return:

Nominal return is the percentage increase in your money without adjusting for inflation.

Real return is the true gain after accounting for inflation.

Example Calculation (June 2025)

Suppose you invest in a 12-month T-Bill with a yield of 10.9274% (SBP Auction, June 2025):

- Nominal Return = 10.9274%

- Inflation = 3.2%

Formula:

Real Return = Nominal Return − Inflation Rate

=10.9274% − 3.2% = 7.7274%

This real return is positive and attractive compared to recent years when inflation exceeded even the highest policy rates.

The Impact of Inflation

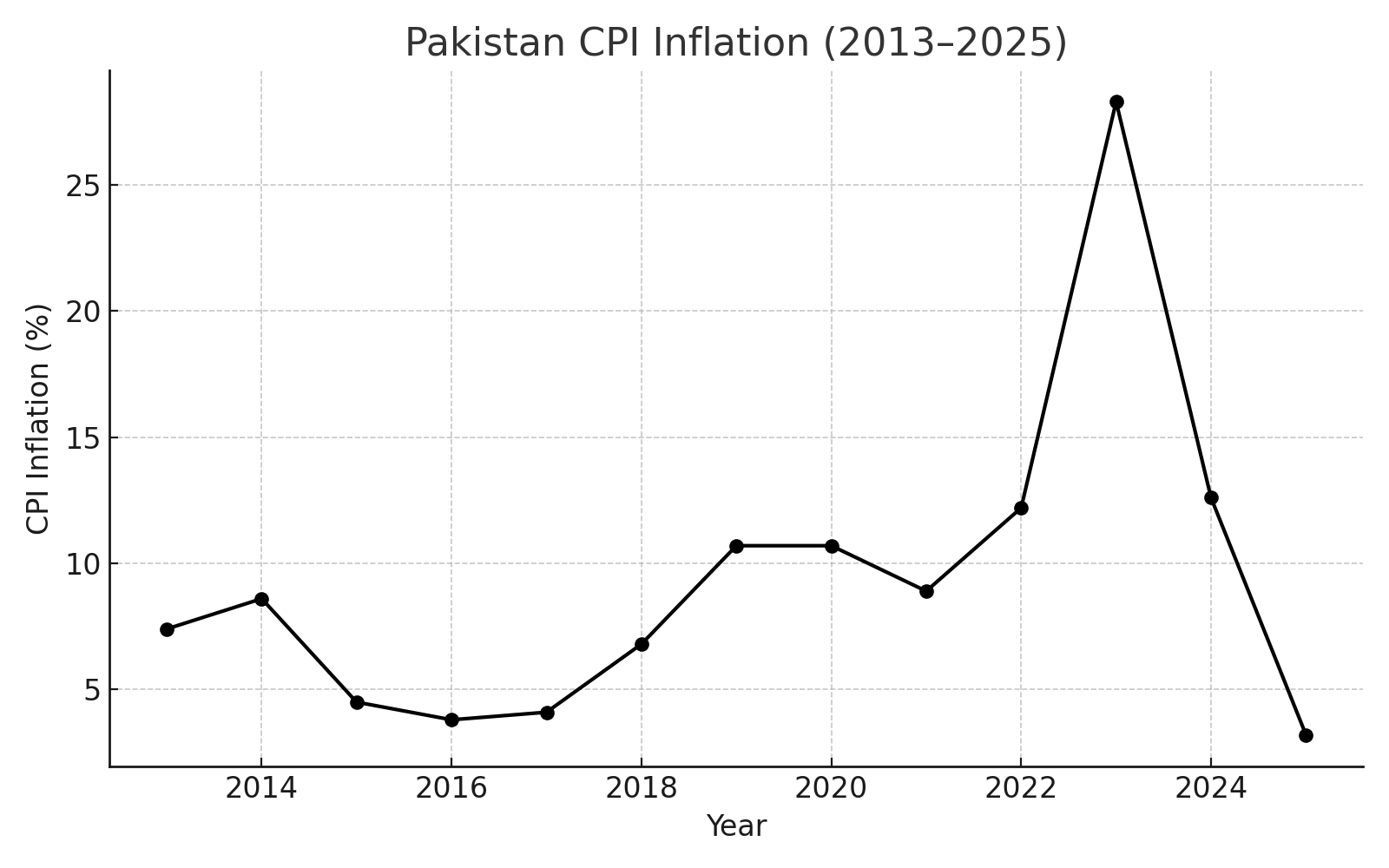

One of the most pressing challenges for Pakistani investors is inflation. Between 2013 and 2025, inflation fluctuated wildly, peaking at 28.3% in 2023 before sharply falling to around 3.2% by mid-2025.

This fluctuation underscores why evaluating returns without adjusting for inflation can be misleading. Because if prices are rising, you can lose purchasing power even if your nominal return seems high. In a country like Pakistan, the real return is a far more accurate measure of investment performance.

Below is verified PBS data for CPI inflation:

| Year | CPI Inflation (%) |

| 2013 | 7.4 |

| 2014 | 8.6 |

| 2015 | 4.5 |

| 2016 | 3.8 |

| 2017 | 4.1 |

| 2018 | 6.8 |

| 2019 | 10.7 |

| 2020 | 10.7 |

| 2021 | 8.9 |

| 2022 | 12.2 |

| 2023 | 28.3 |

| 2024 | 12.6 |

| 2025 (June) | ~3.2 |

Historical data for Pakistan shows that high inflation reduces real returns and creates uncertainty. Inflation often drives currency depreciation and higher interest rates. This increases investment risk and makes achieving stable returns more difficult.

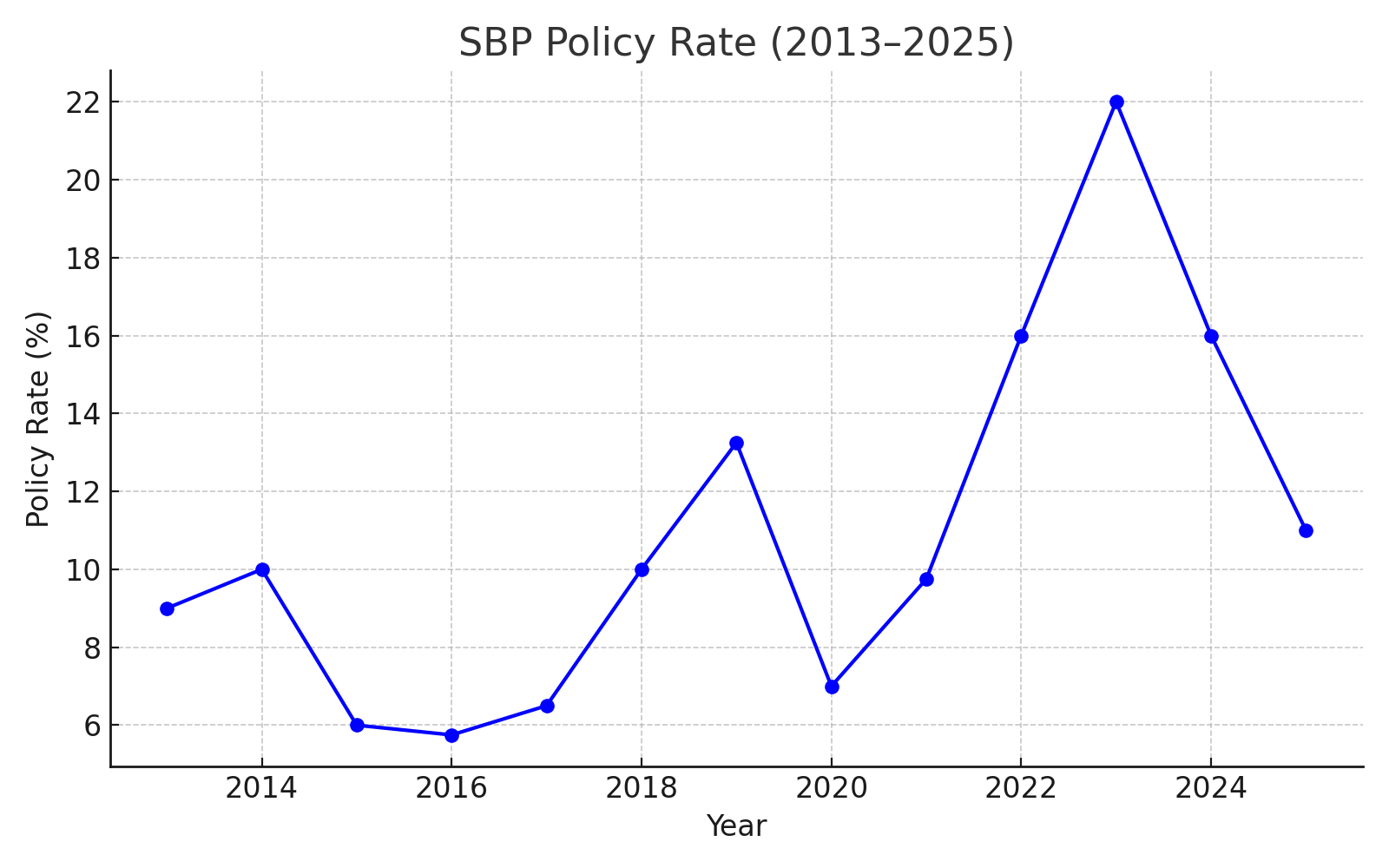

The Policy Rates and Real Returns

In response to inflation swings, the State Bank of Pakistan (SBP) uses its policy rate to cool or stimulate the economy. The policy rate is the interest rate at which commercial banks borrow from the central bank. When the SBP raises this rate, borrowing costs rise, slowing demand and curbing inflation. When it lowers rates, borrowing and spending become cheaper, boosting growth.

In Pakistan’s investment landscape, a higher policy rate raises borrowing costs and dampens business growth, increasing investment risk while making government bonds more attractive. Conversely, a lower rate reduces secure returns, pushing investors toward stocks and real estate. Policy rates therefore directly shape how much risk investors are willing to take.

Below is SBP’s policy rate history:

| Year | Policy Rate (%) |

| 2013 | 9.0 |

| 2014 | 10.0 |

| 2015 | 6.0 |

| 2016 | 5.75 |

| 2017 | 6.5 |

| 2018 | 10.0 |

| 2019 | 13.25 |

| 2020 | 7.0 |

| 2021 | 9.75 |

| 2022 | 16.0 |

| 2023 | 22.0 |

| 2024 | 16.0 |

| 2025 (June) | 11.0 |

These rates influence all lending and deposit rates in the economy. The 22% peak in 2023 was the highest in SBP history, designed to combat the inflation crisis.

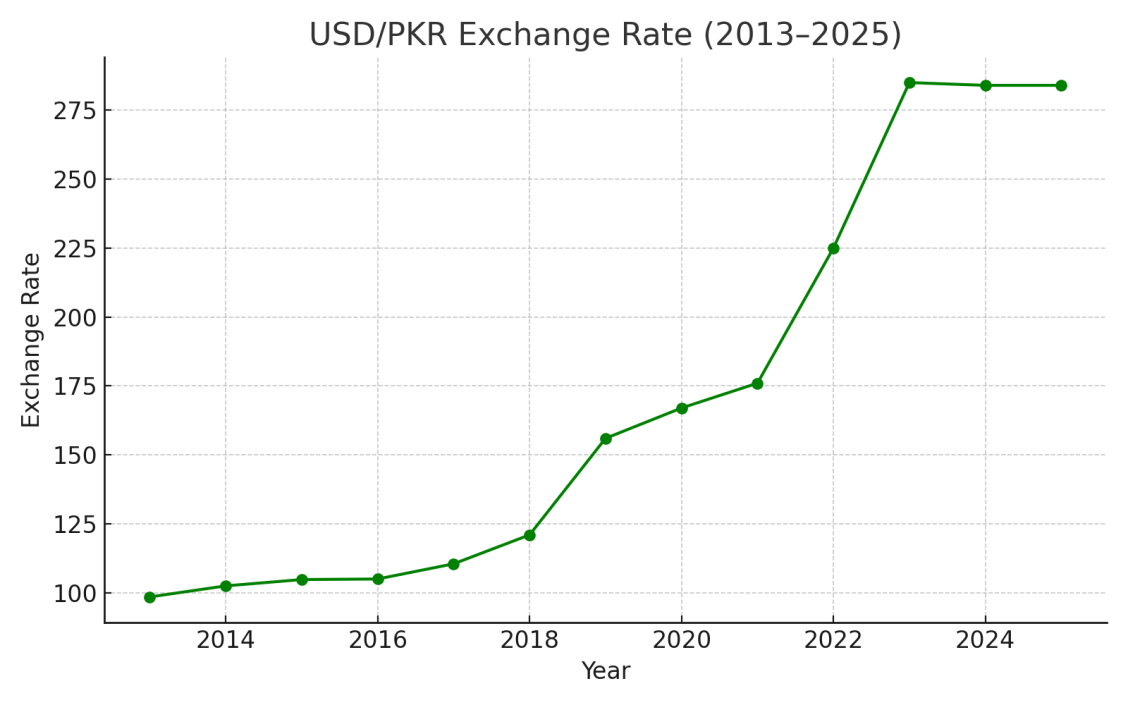

The Currency Fluctuations

Over the long run, the rupee’s loss of value remains one of the defining risks for local investors. Even if local instruments pay attractive rupee returns, they may underperform in dollar terms if the currency weakens further. Investors who ignore currency risk may find that their global buying power is steadily diminishing, even if their rupee portfolio appears to be growing.

The Pakistani rupee’s long-term depreciation has been dramatic. From an average exchange rate of PKR 98.5 per USD in 2013 to approximately PKR 284 in 2025, the currency has lost over 190% of its value. This persistent decline affects purchasing power, particularly for those who need to pay for foreign education, travel, imports, or offshore obligations.

Thus, currency fluctuations increase investment risk by making returns unpredictable for foreign investors. A weaker currency can reduce real returns on assets, while stability supports more reliable, attractive returns.

| Year | USD/PKR Average |

| 2013 | 98.5 |

| 2014 | 102.5 |

| 2015 | 104.8 |

| 2016 | 105.0 |

| 2017 | 110.5 |

| 2018 | 121.0 |

| 2019 | 156.0 |

| 2020 | 167.0 |

| 2021 | 176.0 |

| 2022 | 225.0 |

| 2023 | 285.0 |

| 2024 | 284.0 |

| 2025 (June) | 284.0 |

The Stock Market Performance

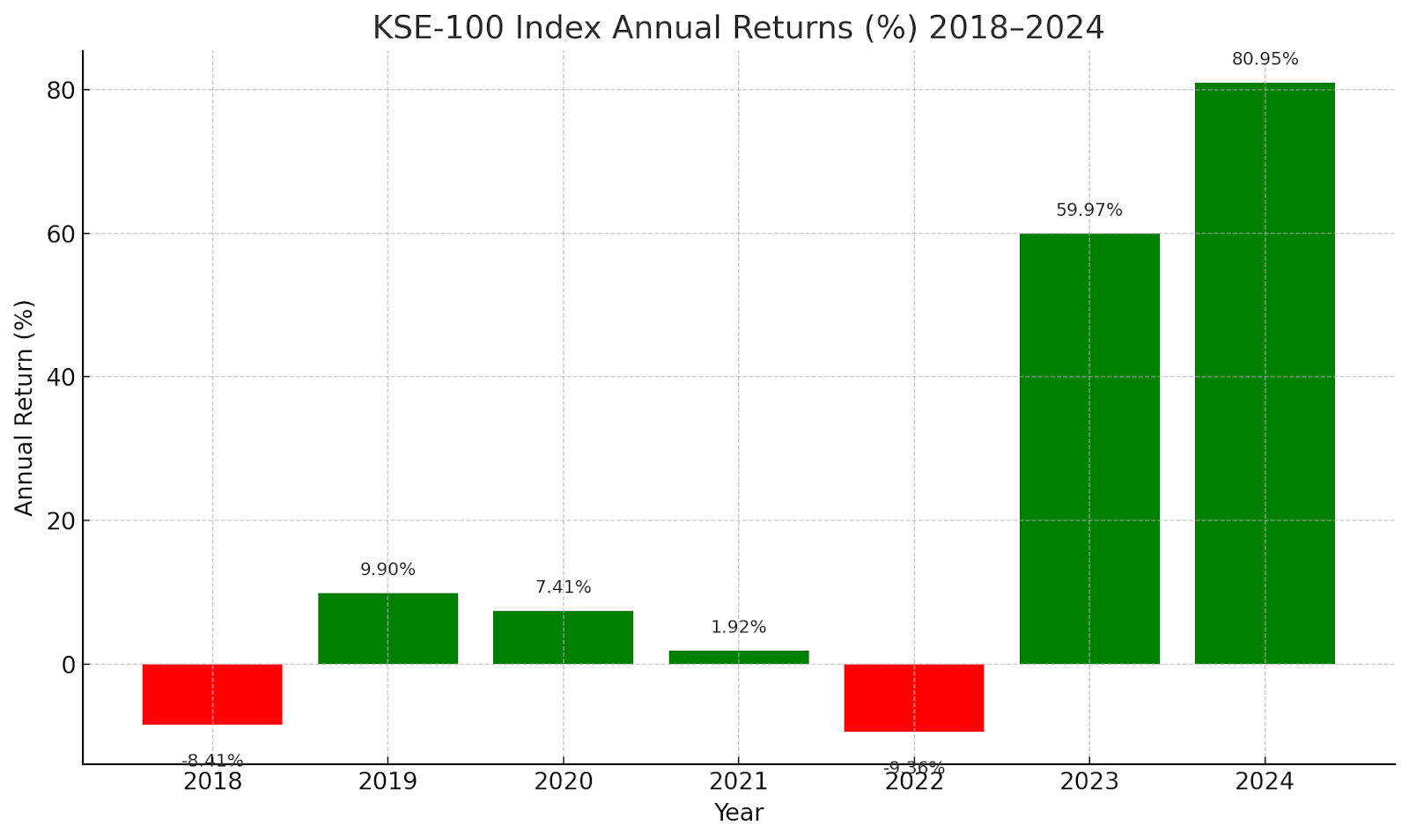

Equities remain attractive for their growth potential. They allow investors to beat inflation and participate in the country’s economic development. However, they require patience and a long-term view. Short-term market movements can be sharp and often influenced by political news or regulatory changes.

The KSE-100 Index vividly illustrates the trade-off between risk and return in Pakistan’s stock market. The PSX’s annual reports show annual returns of +7.4% in 2020, a sharp decline of –9.4% in 2022, and an impressive rebound of +60.0% in 2023 and approximately +85% in 2024. These large swings highlight that while equities can generate substantial returns, they also carry significant volatility. To navigate this, investors often reduce risk through diversification—across sectors, dividend-focused stocks, and solid fundamentals—helping smooth out returns despite periodic market shocks.

Below is the real KSE-100 index annual return data

| Year | End-Dec Close | Annual Return (%) |

| 2018 | 37,066.67 | –8.41 |

| 2019 | 40,735.08 | +9.90 |

| 2020 | 43,755.38 | +7.41 |

| 2021 | 44,596.07 | +1.92 |

| 2022 | 40,420.45 | –9.36 |

| 2023 | 64,661.78 | +59.97 |

| 2024 | 117,008.08 | +80.95 |

Constructing a Balanced Portfolio

Creating a robust portfolio in Pakistan requires a mix of assets that collectively balance risk and return. Based on mid-2025 data, a sample allocation strategy could include the following:

- 40% in government securities (e.g., Treasury Bills, Pakistan Investment Bonds), yielding around 11%

- 20% in National Savings Schemes, providing returns of 15–19%

- 20% in equities, targeting long-term average returns of 15–20%

- 15% in real estate, offering both rental income and capital appreciation (10–14%)

- 5% in gold as a defensive hedge (14–15% historical return)

Weighted average expected return would be

= (0.40×11%) + (0.20×17%) + (0.20×17%) + (0.15×12%) + (0.05×14.5%) =13.73%(Nominal)

Calculating the weighted average expected return yields approximately 13.8% nominal. After adjusting for expected 2025 inflation of ~3.2%, the real return comes out to about 10.6%. Such a portfolio helps mitigate short-term volatility and offers long-term growth, though it still carries exposure to equity market fluctuations and rupee depreciation..

Conclusion

Investing in Pakistan is a challenge, but also an opportunity. With inflation cooling and policy rates normalizing, there is a unique chance to lock in real returns, hedge against risks, and grow wealth in a disciplined manner. Success will depend on how well investors understand the local economic terrain and apply risk management principles.

Ultimately, building a resilient investment portfolio in Pakistan requires more than just luck. It demands careful planning, a long-term view, and a commitment to staying informed. Those who adapt and diversify intelligently can turn volatility into opportunity and navigate Pakistan’s financial markets with confidence.

No responses yet